The Mechanics of Cash on Close in Mid-Market M&A

Cash on close is the focal point for almost every mid-market founder seeking to exit. Yet for as much as it is desired…or even expected by sellers…it typically lands somewhere between 60% and 75% of the total transaction value for most founders selling their business. The challenge is that few founders understand why there tends to be cash limitations in offers. Why won't a buyer simply offer all cash? Why is 60% to 75% often the ceiling rather than the floor? And why, the part almost no one is told, is an all-cash offer usually not the most competitive one on the table?

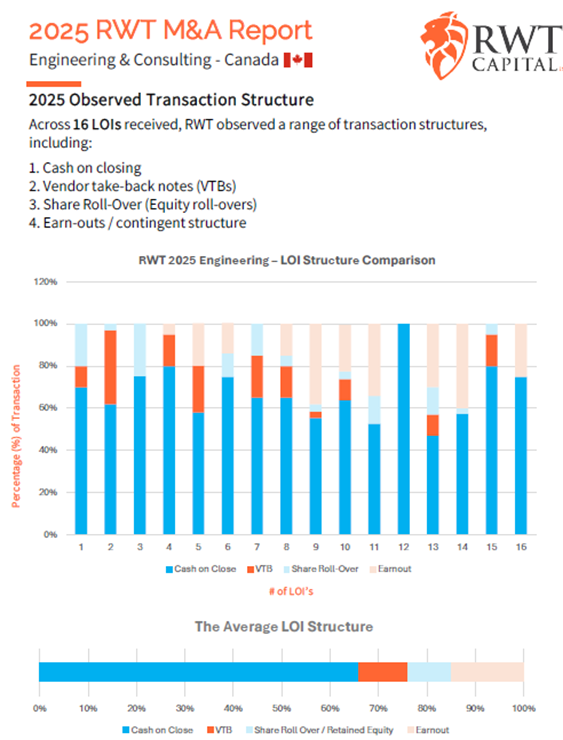

Below is an example of LOIs received by RWT for engineering clients in 2025…you can clearly see the cash on close trends.

To understand the potential cash ceiling, you have to understand how buyers actually make their returns. Unless the deal is highly strategic and is being performed by a buyer sitting on copious amounts of cash or a strong acquisition line (a piece for another article), cash paid on close is almost always a combination of money the buyer has borrowed from a lender and capital the buyer puts in themselves. This is especially true in private mid-market deals. Buyers lean on debt because it is more available and cheaper than equity, and they limit how much of their own capital goes into a deal because that capital is harder to raise and more expensive to use. Equity is costly because it means giving up a piece of the company, or the deal, to investors…and that cost is usually far higher than the cost of debt. For better or worse, this is how buyers arrive at the amount of cash they are willing to commit.

The constraint that sets the ceiling is the lender. In Canada, a lender will typically advance somewhere between 2x and 3x EBITDA against a stable, cash-generating business (in the US this can be much higher…thank the Canadian banking system for this). On a company changing hands at a 5x multiple, that means debt covers only 40% to 60% of the purchase price. The rest of the cash has to come from the buyer's own pocket. This is exactly where the cash disconnect between buyer and seller arrives. When a seller receives an offer with 75% cash on close, the buyer is funding 15% to 35% of the total price with their own capital…the gap between what the lender will advance and what the seller wants at close.

That buyer equity is the expensive, nervous money in the deal. It sits behind the lender, it carries a higher cost than the debt stacked in front of it, and it only earns a return if the business performs. So the buyer has to be genuinely confident they can grow the company, or be willing to watch their own capital sit idle and at risk. The more cash a seller demands at close, the more of this expensive equity the buyer has to commit, and the thinner the deal's returns become. A vendor take-back…or an earn-out or share roll over…exists in part to relieve exactly this pressure: it reduces the equity the buyer has to put in today, while deferring a portion of their return.

But the deferred portion is doing something more important than filling a financing gap, and this is the part a founder needs to sit with. When a buyer asks you to carry a vendor take-back, they are asking you to lend part of the price back to the deal and wait behind the bank to be repaid. They are doing this because they cannot fully verify your story before close. They are underwriting your representations as a seller…that the customers don't leave, the profit margins hold, the earnings normalize the way your adjustments suggest. The VTB is how a buyer bridges the one thing they cannot confirm until after the deal is done: whether the business performs the way you say it will, under their ownership, well enough to pay you back. The deferral is not the buyer taking something from you. It is the buyer reducing uncertainty for themselves via cash preservation.

Which sets up the part most founders never hear until it is too late: the all-cash offer can be the worst offer on the table, even though it feels like the best one.

Consider the buyer who is willing to pay 100% cash on close. That buyer has to absorb 100% of the risk on day one, with no recourse if the business underperforms. They cannot claw anything back. They cannot tie any part of the price to the customers staying or the earnings holding. So they do the only rational thing left to them…they protect themselves on price. They pay less in total, because the certainty of all cash has to be bought somewhere, and the place they buy it is your multiple. While this isn't always true however. We recently sold a business for all cash, and it was the best offer on the table…that was a highly strategic deal for a very well-funded buyer, where paying all cash made complete sense. Most of the time, it doesn't work this way. We have received many all-cash offers that were markedly lower than other offers on both cash at close and total transaction value. Sometimes shockingly lower…so this is an issue that needs to be handled with caution and care.

In comparison, a structured offer does the opposite. When a buyer is willing to defer part of the consideration, they are usually willing to pay more in total, because the structure is protecting them instead of the price. So the deferred consideration is really a question being asked of you: do you believe your own numbers? If you do, the VTB can be construed not as risk you are absorbing, but as money you fully expect to collect, on top of a higher headline price. The founder who fights to convert that structure into cash is often fighting to be paid less in exchange for the feeling of certainty.

Let me make this concrete, because the abstract version of this argument never changes anyone's mind. Imagine two offers for the same company, one generating $2M of EBITDA.

The first is all cash at 4.5x…$9M, all of it on close. Clean, certain, done. The second is structured at 5.5x…$11M in total, with 70% in cash on close and the remaining 30%, a little over $3M, deferred through a VTB.

The all-cash founder takes home $9M and sleeps well. The structured founder takes home $7.7M on close...less on day one…and then, as the business carries on and the note is repaid, collects the remaining $3.3M, for $11M in total. That is $2M more, better than a 20% difference in lifetime proceeds, for accepting structure on a business they presumably believe in.

Now run the unkind scenario. Say the business falters completely and the buyer can only repay half the VTB. The structured founder still collects $7.7M on close plus roughly $1.5M…about $9.35M. Still more than the all-cash deal, even in the bad case. To be clear, across all the deals we have been a part of, we have seen a VTB go unpaid in full only once.

That is the whole argument in one example. The structured deal wins clearly if the business can repay the debt and roughly ties if it horribly disappoints. The only world in which all cash was the better choice is one where the founder secretly did not believe the company would hold up at all…in which case the better question is whether they should have been representing those numbers in the first place.

So the number to negotiate was never the cash-on-close percentage. It was the structure underneath it…and your expectations and understanding of how the cash-on-close element actually works in M&A. The founders who understand that walk away with more…and the ones who fixate on the close-day figure too often pay for that certainty with the very thing they were trying to maximize.

Reece Tomlinson is the Founder and CEO of RWT Capital Corp. and is the author of Uncommon Capital.